We initiate coverage on ASK Automotive Ltd with a BUY and a Target Price of Rs 550. ASK ’s promising outlook is underpinned by its ability to

(i) outpace industry growth,

(ii) expand wallet share with OEMs,

(iii) increase its export footprint and

(iv) huge growth potential of the ALPS business, aided by foray into differentiated alloy wheels business.

With its market leadership position in the ABS segment offering stability, ASK has shown strong technical expertise by achieving a 35% CAGR in fast-growing ALPS business over FY21-25. The company is strategically well-placed to benefit from the electrification wave, supported by higher content per EV compared to ICE vehicles and marquee EV clientele. ASK has the potential to get rerated as scale expands, margins improve meaningfully, exports pick up, high return ratios and best in class cash conversion cycle sustains along with impressive CFO/EBITDA conversion.

ASK holds a leading 50% market share in India’s 2W brake-shoe and advanced braking segment (ABS), covering both OEM and branded IAM segments. It has established enduring relationships with the top 2W OEMs, spanning over two decades, underscoring its strong customer stickiness and strategic relevance in the value chain as a critical safety component. With nearly 75% of the 2W industry still dependent on drum brake systems, we believe the significant cost differential between drum and disc brakes will continue to favor drum brake adoption, an area where ASK maintains clear leadership. This well-established and mature business line is slated to witness 8-9% CAGR - in line with the underlying 2W industry.

ASK has strategically capitalized on the industry-wide lightweighting trend, leveraging its in-house design capabilities and tooling expertise. It has benefited from multi-vendor sourcing strategies adopted by major Indian OEMs, enabling it to expand wallet share within key accounts. ASK ’s timely diversification into EV-specific parts and higher content per vehicle mitigates the risk from EV transition faced by certain engine components. Further, ASK ’s entry into alloy wheels backed by HPDC technology offers a potential first-mover advantage. This initiative is supported by strategic collaborations which we expect to unlock a new growth area.

We build in revenue/ EBITDA/ PAT growth of 15%/ 20%/ 22% over FY25-28E on the back of (i) wallet share gains with non-Honda OEMs, (ii) improvement in exports, (iii) contribution from new alloy wheels business and (iv) gradual increase in industry EV penetration. ASK should achieve a 170bps margin expansion by FY28E, driven by the ramp-down of its wheel assembly business and higher capacity utilization at new plants. With a presence in ~80% of the organized 2W EV market comprising clients such as TVS, Ola, and Ather, ASK can effectively capitalize on rising EV penetration and new model launches. Financials are robust and are expected to further improve with growth consistently outpacing the industry, margins > 13.5%, return ratios > 20%, CFO/EBITDA conversion > 70%, and one of the industry’s best cash conversion cycles at just 14 days by FY28E.

ASKs positioning in the ABS segment and steadfast growth in ALPS segment has attributed to a superior 24% CAGR in revenue over FY21-25, also outpacing 2W industry growth at 7-8%. Favorable sectoral tailwinds in the two-wheeler industry coupled with increasing emphasis around light weighting of vehicles and EVs bodes well for ASK . We have valued at 27x 1QFY28E earnings (in-line with its 1-yr forward avg. PE since listing) to arrive at a TP of Rs550. Operational catalysts (pick up in margins, commencement of alloy-wheel business and gradual client diversification) could well see valuation multiple expand further. Key Risks: High client concentration, failure to ramp up exports and delay in contribution from the alloy wheels business.

Rating: BUY

CMP: INR 471 | Target Price: INR 550

Upside: 17 %

Click to download the full Ask Automotive IC Report

Analyst: Smit Shah (NISM – 202300068297)

Company website: https://askbrake.com/

Disclaimer: You are advised to read our disclaimer here: Click to view

Empower your finances with ReSach – the stock trading apptrusted by serious investors. Whether you're planning to invest in stocks, explore commodity trading, or need a financial advisor to guide you, Resach brings it all under one platform.

Start trading today with ReSach and unlock seamless investing on the go.

Name of the Company has changed from Networth Stock Broking Limited to Monarch Networth Capital Limited upon Certification of Incorporation received from Registrar of Companies, Mumbai vide certificate dated 13th October, 2015.

If you are not satisfied with the resolution provided, you can lodge your complaint online at: https://scores.sebi.gov.in/link

In case of grievance client can log on to the SMART ODR Portal, if they are unsatisfied with the response provided by us. Your attention is drawn to the SEBI circular no. SEBI/HO/OIAE/OIAE_IAD-1/P/CIR/2023/131 dated July 31, 2023, on “Online Resolution of Disputes in the Indian Securities Market”.

Purchase of REs only gives buyer the right to participate in the ongoing Rights Issue of the concerned company by making an application with requisite application money or renounce the REs before the issue closes. REs which are neither subscribed by making an application with requisite application money nor renounced, on or before the Issue closing date shall lapse and shall be extinguished after the Issue closing date. Please check your dp account for further details.

Please do not share your online trading password with anyone as this could weaken the security of your account and lead to unauthorized trades or losses.

Monarch Networth Capital Limited (‘MNCL’) | CIN No.: L64990GJ1993PLC120014

Unit No. 803-804A, 8th Floor, X-Change Plaza, Block No. 53, Zone 5, Road-5E, Gift City, Gandhinagar - 382050, Gujarat

Ahmedabad

“Monarch House”, Opp Prahladbhai Patel garden, Near Ishwar Bhuvan, Commerce Six Roads, Navrangpura, Ahmedabad - 380009

Mumbai

Monarch Networth Capital Limited, G Block, Laxmi Tower, B Wing, 4th Floor, Bandra Kurla Complex, Bandra East, Mumbai - 400051.

Email for Grievance: grievances@mnclgroup.com

Investors are requested to note that Stock broker (Monarch Networth Capital Ltd) is permitted to receive money from investors through designated bank accounts only named as Up streaming Client Nodal Bank Account (USCNBA). Stock broker (Monarch Networth Capital Ltd) is also required to disclose these USCNB accounts to Stock Exchange. Hence, you are requested to use following USCNB accounts only (Click to View) for the purpose of dealings in your trading account with us. The details of these USCNB accounts are also displayed by Stock Exchanges on their website under “Know/ Locate your Stock Broker".

Mechanism for addressing grievances and information about SCORES.

Monarch Networth Capital IFSC Private Limited (Wholly owned subsidiary of Monarch Networth Capital Limited) is a Registered Fund Management Entity (Retail) having Registration No: IFSCA/FME/III/2025-26/169. Monarch India Growth Fund will be an open-ended Restricted Scheme (Non-Retail) construed as a Category III AIF under the IFSCA (Fund Management) Regulations, 2025. Monarch AIF is a Category III AIF having SEBI Registration No. IN/AIF3/20-21/0787. This material is for informational purposes only and is not intended as an offer or solicitation or investment advice to buy or sell securities. Investments are subject to market risks. The offering is made only through official scheme documents to eligible investors under GIFT IFSC regulations. Investors should read all documents carefully and consult their advisors before investing.

Mechanism for addressing grievances and information about SCORES.

Monarch Networth Capital Limited (‘MNCL’) | CIN No.: L64990GJ1993PLC120014

(As per LODR Regulations and Companies Act, 2013)

Contact information of the designated officials of the listed entity who are responsible for assisting and handling investor grievances : Mr. Nitesh Tanwar

Monarch Networth Capital Limited

Unit No. 803-804A, 8th Floor, X-Change Plaza, Block No. 53, Zone 5, Road-5E, Gift City, Gandhinagar - 382050, Gujarat

Ahmedabad

“Monarch House”, Opp Prahladbhai Patel garden, Near Ishwar Bhuvan, Commerce Six Roads, Navrangpura, Ahmedabad – 380009

Mumbai

Monarch Networth Capital Limited, G Block, Laxmi Tower, B Wing, 4th Floor, Bandra Kurla Complex, Bandra East, Mumbai - 400051.

Phone: 022 - 66476400 / 66476405

Email: cs@mnclgroup.com

Email for Grievance: cs@mnclgroup.com

Listing of Equity Shares on Stock Exchange at

BSE

NSE

(Formerly known as Link Intime India Private Limited)

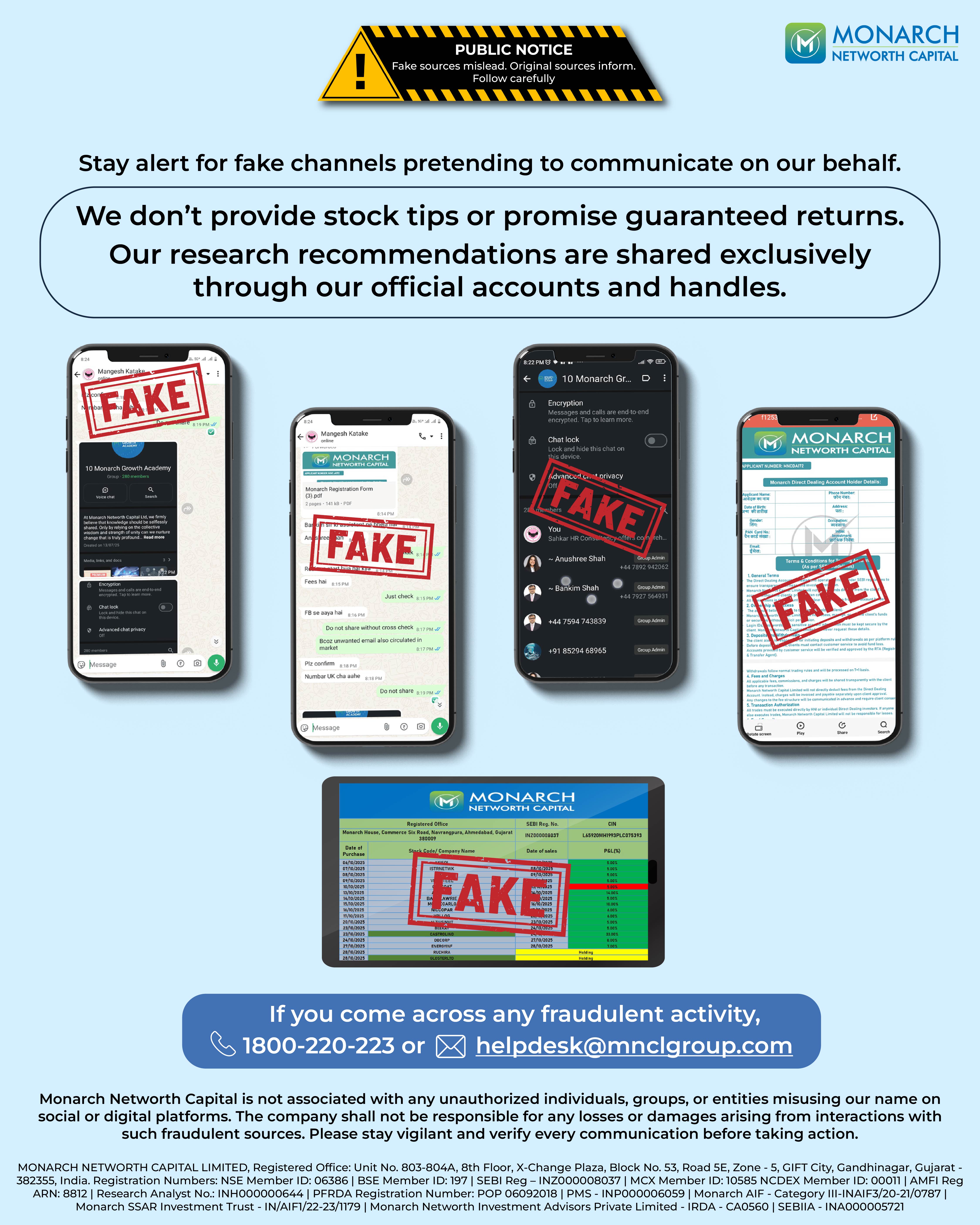

For any queries related to broking please contact helpdesk@mnclgroup.com.

‘Investments in securities market are subject to market risks, read all the related documents carefully before investing.’